Buying a Business, Selling a Business

Anatomy of a dumb deal – by business buyers

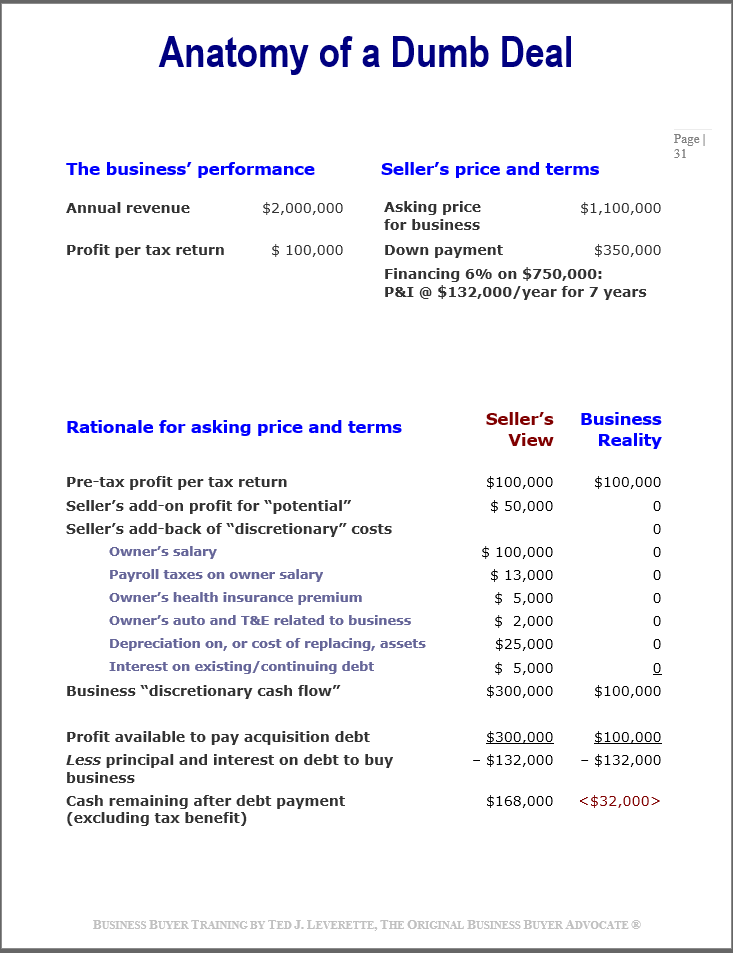

This graphic (from an early edition of the syllabus I give to people attending my Zoom Business Buyer Trainings) hasn’t changed in decades, other than the numbers have gotten bigger.

And so has the risk, for business buyers who don’t know how to properly adjust and forecast financial statements and/or cope with the wishful thinking of business sellers.

Those kinds of errors adversely affect valuation and dealmaking, don’t they?

It’s not surprising that the financial profile of the company in the example is similar to the offering terms of businesses for sale advertised in the online marketplaces.

- Business buyer competition heaven, for sellers.

What is surprising is how many buyers believe the seller’s view – and then agree to the (ridiculous) price and financing this example depicts.

Sellers are delighted by eager, uninformed competition among buyers. That’s why street-smart buyers expand their search into the hidden market, where most of the best businesses are sold – off-market – where there is little, if any, buyer competition.

The company in the example is worth buying. It earns a profit in addition to paying the owner a fair management salary and perquisites.

However, if this buy/sell transaction pricing/financing scenario depicts the purchase of the company, the buyer will quickly find himself reaching into his pocket to pay for the business. Why?

- The buyer foolishly agrees to pay the balance due on the price with payments greater than 50% of after-tax profit.

What about price? Only a naive buyer of a privately held company would value the business based upon its potential. Potential is the reason for buying, but not a basis to set a price.

- In computing profit, the business’ “discretionary” costs are not optional unless the buyer wants to forego the management salary and perks of ownership, to risk insolvency.

A buyer risks a cash flow crisis if he fails to realize that principal payments are not a tax-deductible expense; they consume cash.

- That’s why it is important to compute after-tax profit – to see how much cash is available to make principal payments on acquisition (and other) debt.

Here’s some of what I can bring to your side of the dealmaking table if you include me on your advisory team:

I’m The Original Business Buyer Advocate ®. I’m not a business broker; never have been.

For more than 30-years, over 100,000 entrepreneurs and advisors, worldwide, have relied upon my books and trainings to creatively finance, buy, or sell small and midsize businesses. I’ve privately coached more than 1,000 clients. And, I’ve trained 298 independent advisors, so they can better-serve people buying and selling businesses.

- But I can’t unscramble eggs, so let’s collaborate before things get messy for you.

This is the first valuable deliverable I provide for people wanting to find and buy the right businesses the right ways: Targeting the best opportunities and then finding them.

It comes down to this: How good or bad do you want your experience to be when buying or selling a business (or when you advise your clients)?

- To know (enough) or not to know? That is the question.

Read my book: How to Buy the Right Business the Right Way—Dos, Don’ts & Profit Strategies.

Improve your search and dealmaking:

Schedule an hour of coaching with Ted Leverette, The Original Business Buyer Advocate ®

Email Ted J. Leverette, The Original Business Buyer Advocate ®. “Partner” On-Call Network, LLC

![]()